By Musabbir Mazhar

[I wrote this Equity/Stock Research Report on July 7, 2017; the company subsequently got acquired but thought I would post it to share some of my valuation thought process]

About the Company

ZCL Composites Inc. manufactures and supplies underground storage tanks (UST) made from environmentally friendly fiberglass reinforced plastic (FRP). The company is the largest player in North America in this business. The purpose of the business is to provide corrosion resistant solutions for tanks that protect the environment. The company was established in 1987 to supply fiberglass underground fuel storage tanks in Canada and in 1989 manufactured the first double-wall fiberglass tanks. The company has 7 plants: 2 plants in Canada, 4 in the US and 1 in The Netherlands. ZCL generates revenues through 3 main business segments (by products):

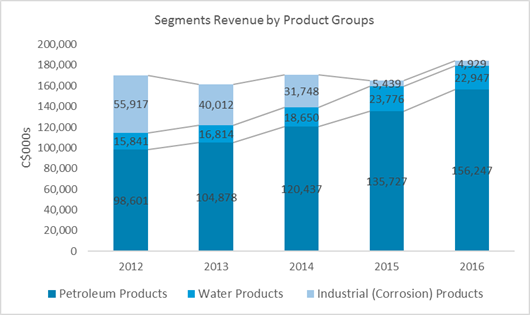

- Petroleum Products (84.9%)

- Water Products (12.5%)

- Corrosion (or Industrial) Products (2.7%)

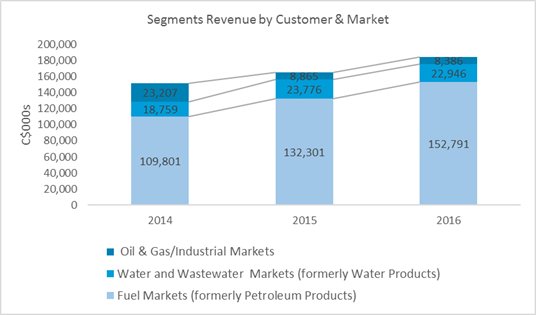

As of 2017 Q1, the company has decided to report segments based on customers and market approach as opposed to product groups historically reported. ZCL’s revenues through 3 new main business segments (by markets):

1. Fuel Markets (formerly Petroleum Products) (83%)

2. Water and Wastewater Markets (formerly Water Products) (12.5%)

3. Oil & Gas/Industrial Markets (4.6%)

Executive Summary:

Business Model & Outlook (Fuel, Water, Oil):

- North American leader in manufacturing fiberglass reinforced underground storage tank

- Well-positioned in industry to take advantage of concerns regarding use of aging steel tanks

- Economic moats via market share, far-reaching north American presence

- Diversification through types of customers and markets and geography

- High growth prospects in North American waste water markets and in US fuel markets

- Higher demand for ZCL’s tanks and services due to environmentally friendly offering and thus backed by regulatory support

Balance Sheet Overview:

- ZCL has strong liquidity position with good Free Cash Flow

- The company has debt-free capital structure

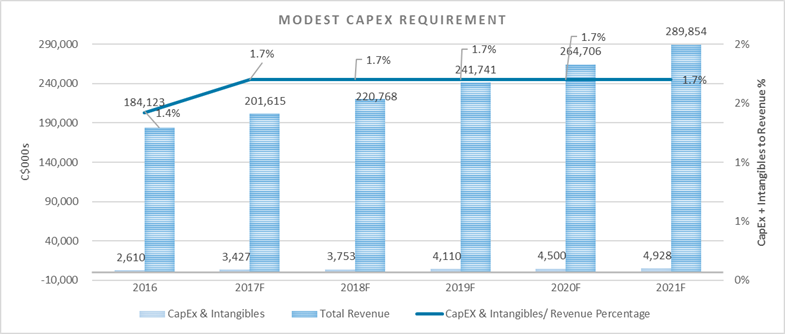

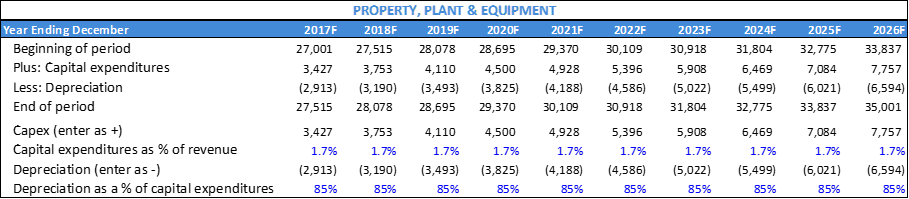

- Modest CapEx requirements ~1.7% of revenues

Returns Profile:

- Good shareholder return prospects with high historic and high expected annual growth rates in revenues, earnings, prominent sustainable ROIC and dividend payout

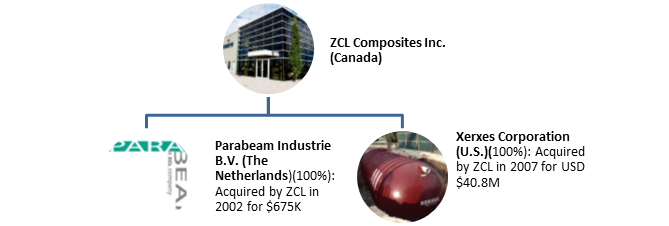

Intercorporate Relationships:

- Several subsidiaries in US, Canada, and international formed as a result of acquisitions

Key People:

- Run by experienced, loyal people invested in the company’s shares

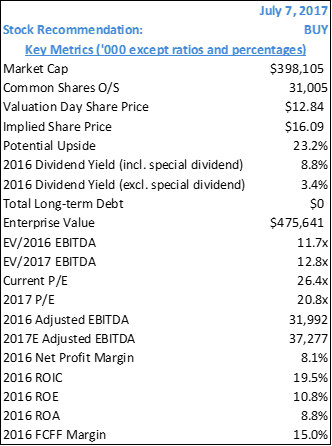

Valuation:

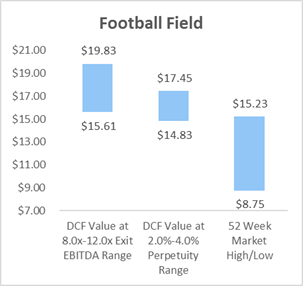

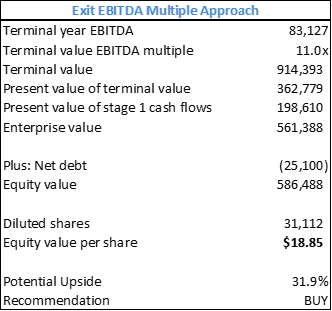

- Perpetual LTG DCF estimates a target share price of $16.09 with ~20% upside and a total return of 23%; which is also supported by EV/EBITDA Exit-Multiple of 11x at $18.85 with a 32% price upside potential and a total return of 35%.

Risks & Challenges:

- Fuel market concentration; damped oil price, regulatory outlook, cyclical long-term growth viability

Business Model & Outlook

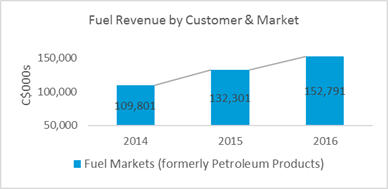

1. Fuel Markets (formerly Petroleum Products) (83%):

Fuel Product:

Fuel markets is ZCL’s main segment and revenue is generated by selling underground storage tanks for storing gasoline and diesel fuel for downstream retail outlets in US & Canada. It is a leader in this market in supplying mostly double-wall tanks (ranging from 2,500 liters to 200,000 liters) with availability of single and triple wall models as well. The double wall tank allows continuous monitoring which is not available to steel tanks.

ZCL, in addition, provides in-place upgrades of steel or fiberglass tanks via a second container tank system or stand-alone double wall tank system – this is called the Phoenix System.

ZCL also generates revenue through international 3rd party technology licensing agreements and sale of Parabeam, which is a three-dimensional glass fabric.

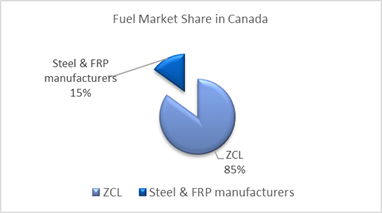

Fuel Market Share & Economic Moat:

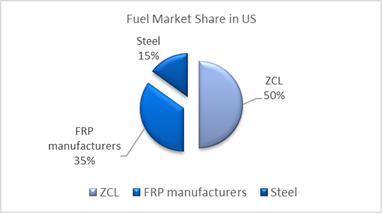

The estimated target market size of downstream retail service station in Canada is $25M to $35M, where ZCL has over 85% market share. The remaining market share is occupied by steel and other FRP tank manufacturers.

The estimated target market in US is $200M to $250M, where ZCL as over 50% of market share of the FRP and steel combined. The total UST market in US is comprised of 85% to 90% FRP tank manufacturers while the rest belongs to steel manufacturers.

The company is able to provide competitive pricing and fastest delivery times due to its broader geographical presence in north America and hence shipments take place directly from manufacturing plants to final installed location, supported by internal sales force and independent sales agents and distributors.

In addition to having experienced industry personnel who are loyal, the company has robust brand presents including ZCL, Xerxes, Parabeam; patents and repeat diversified customer base. Only 1 customer represents more than 10% of Accounts Receivable whose collectability has no concerns.

Fuel Customers, Current Market & Growth Target

ZCL’s key customers comprise:

- Gas station

- Convenience store

- Truck stop operator

- Equipment distributor

- Trucking company

- Car rental agency

- Utility

The company is in a mature stage in this segment, more so in Canada, while in US, there are growing opportunities with US big box retailers entering the retail fuel markets via gas stations. In Canada, conditions look to have improved since the 2014 oil crash and reduction in spending.

The company has had CAGR of 13% in last 5 years in fuel markets. The management expects future growth in high single digits annually.

The company looks to grow revenues from new downstream retail store openings and increasing tank replacement of both steel and FRPs. This is triggered due to:

- Aging tanks

- End of warranty of 1980’s tanks

- Environmental ill-effect concerns due to potential leakage

- State regulation

- Risk management motive

- Insurance converge clause and bank constraints

There is increasing opportunity for the company by gulping the decreasing steel tank market share from both existing and newer opportunities (steel accounts for less than 15% of new installations as management estimates). This is since there is larger acknowledgement that new fuels and biofuels lead to internal corrosion to steel tanks and hence the replacement need since these fuel types are more environmentally friendly and the future.

The company targets to replace over 300,000 in service steel USTs in north America since estimates say there about 110,000 tanks older than 30 years and 340,000 tanks older than 20 years. To get perspective, there are approximately 558,000 regulated active USTs (at approximately 201,000 sites). Currently about 7,500 USTs are sold in north America.

Fuel Competition:

- Containment Solutions Inc. (CSI), a private company based out of Texas is perceived as the biggest competitor to ZCL in the US FRP tank market

- L. F. Manufacturing, Inc. (LFM), headquartered in Texas is another key manufacturer of FRP structures operating since 1974, currently has 6 manufacturing plants in US

- ZCL faces competition from a number of steel tank manufacturers including Modern Welding, Highland, Northern Steel, and other regional players

2. Water and Wastewater Markets (formerly Water Products)(12.5%):

Water Product:

Water and wastewater is the 2nd largest revenue generating segment where revenue is generated by selling FRP storage tanks used for:

- Water conservation such as rain/storm water collection and filtration

- Fire protection

- Wastewater treatment and collection

- Industrial wastewater usage

- Plumbing engineered solutions

- Potable water storage

These single-wall tanks are best alternative to concrete tanks which have dominated the market historically. ZCL’s tanks, in addition to being cheaper and less time consuming to install, are better than concrete since concrete is prone to cracking and corrosion.

Water Market Share:

The estimated market size is $400M to $500M in North America with market segments varying from $20M to $100M.

The company has a small market share in this segment.

Water Customers, Current Market & Growth Target:

Key water customers include:

- Developers of water storage and wastewater systems for various residential, commercial and industrial developments

- Engineering, procurement and construction companies

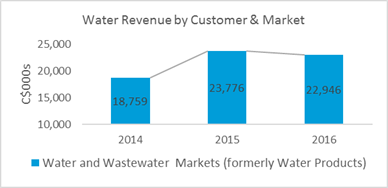

The company has had CAGR of 9% in last 5 years in water markets. However, water and wastewater has the largest prospective growth rate of 10% to 20% annually, as company expects.

Water Competition:

ZCL’s FRP competitors include CSI, LF, Canwest, Barski, Granby (Nemo) and smaller manufacturers. The company’s polyethylene based products competitors include Norwesco, Darco, Infiltrator and other manufacturers.

Water Customers, Current Market & Growth Target:

Key water customers include:

- Developers of water storage and wastewater systems for various residential, commercial and industrial developments

- Engineering, procurement and construction companies

The company has had CAGR of 9% in last 5 years in water markets. However, water and wastewater has the largest prospective growth rate of 10% to 20% annually, as company expects.

Water Competition:

ZCL’s FRP competitors include CSI, LF, Canwest, Barski, Granby (Nemo) and smaller manufacturers. The company’s polyethylene based products competitors include Norwesco, Darco, Infiltrator and other manufacturers.

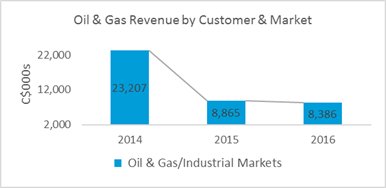

3. Oil & Gas/Industrial Markets (4.6%):

Oil & Gas/Industrial Product:

This segment generates revenue by selling underground and aboveground storage tanks, piping, drain tanks and accessories for upstream and midstream markets.

One subsection called industrial markets are served by producing tailor-made FRP products for following uses:

- Chemical processing

- Municipal Wastewater treatment

- Mining

- Pulp and paper

- Agriculture

- Pharmaceutical

- Food processing markets

Oil & Gas Market Share:

There are many companies in the FRP industry in the industrial markets who compete at product level or end market segment level. The company puts its effort in Western Canada and Western US where it believes it can maintain its competitive moats.

Oil & Gas Customers, Current Market & Growth Target:

Key customers include:

- Midstream oil and gas sector companies such as pipeline companies

- Upstream oil and gas sector companies such as producers of crude oil, oil sands, natural gas for storage,

This market has seen a compounded annual revenue growth of 28% and average growth of 4%. However, Management believes this segment will grow at 8%‐10% annually for the long term.

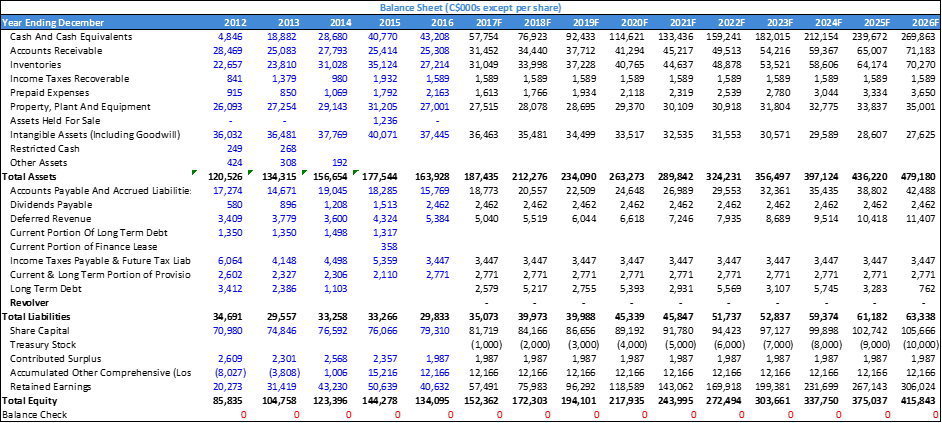

Balance Sheet Overview

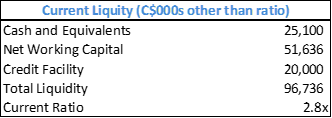

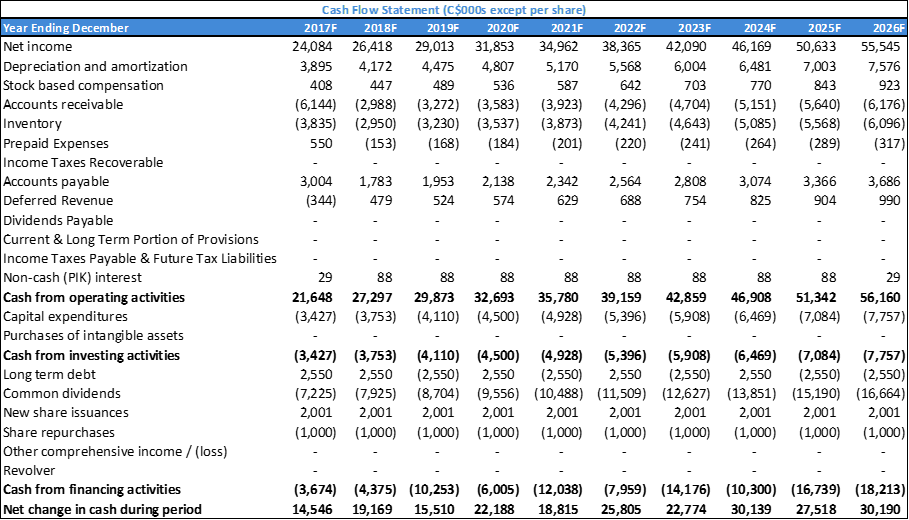

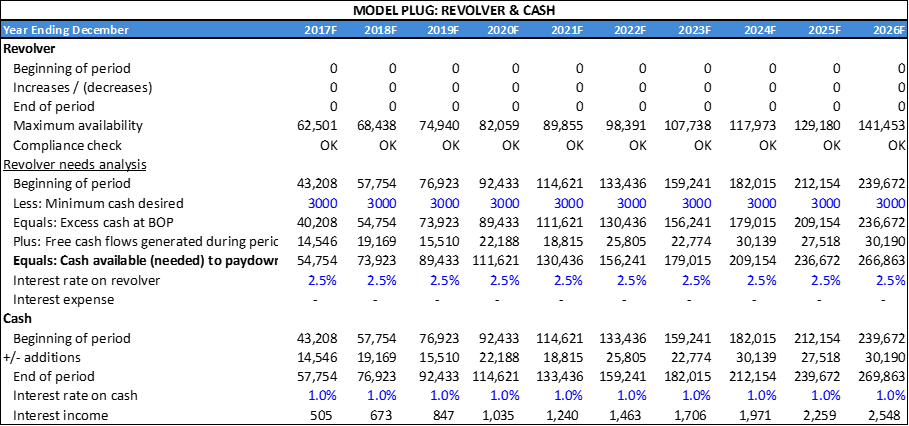

ZCL has zero debt and $25.1M in cash which means it has less risk of financial distress, making its balance sheet quite lucrative. It has an estimated Free Cash Flow to Firm (FCFF) of $27.5M (15% FCF Margin) for 2016 with a 5.3% CAGR forecasted for the next 10 years. The company has a descent current ratio of 2.8x as of Q1 2017 with a high 5 year average of 3.5x. Given total liquidity measure of $96.8M as illustrated and modest CapEx spending, strong FCFF and robust Dividend Coverage ratio, it can be expected that regular operations would be unimpeded from a liquidity standing.

Returns Profile

In 2016, ZCL had a capital return of 45% and 8.8% dividend yield including special dividend, with a total return of 53.8%, showing both market and management’s confidence in the future income generating ability of the company.

The company has a 5Y average Net Income margin of 8.5% and a sustainable forecasted Net Income margin.

ZCL had a very attractive historical 5Y average ROIC of 18.9% which measures the profitability of the capital invested by the company’s shareholders and debt holders; the company has a 10Y forecasted strong fundamental return profile of 15.5%.

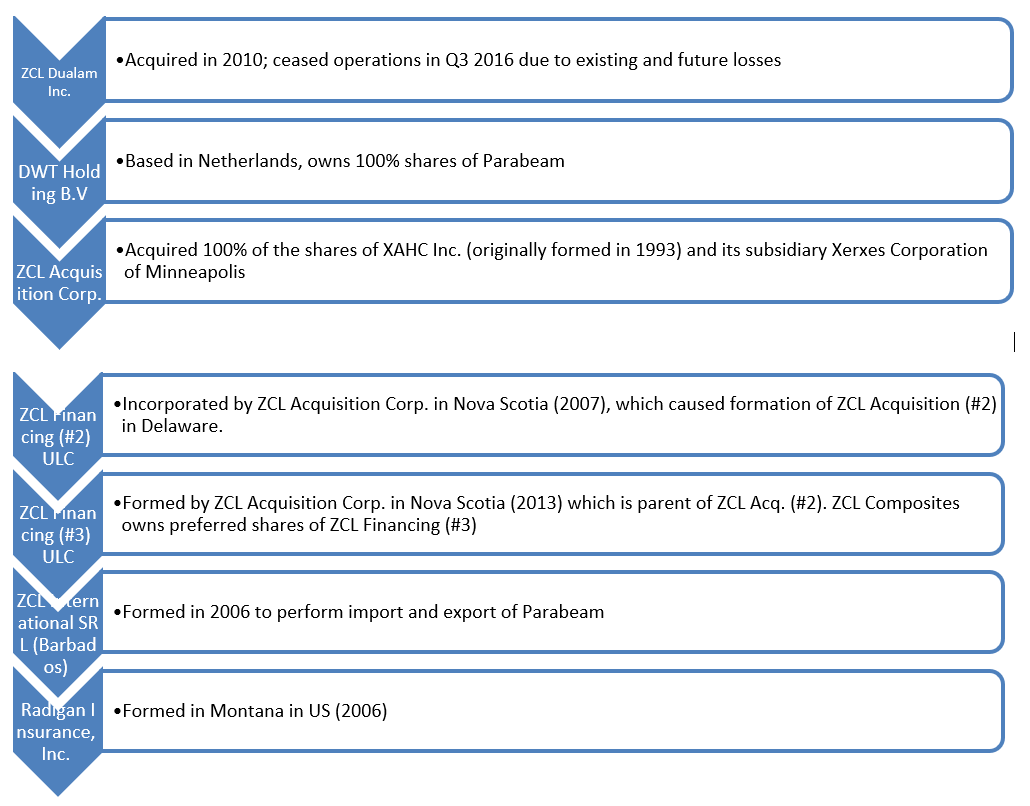

Intercorporate Relationships

Other wholly owned subsidiaries of ZCL whose assets and operating revenues constitute less than 10% of ZCL’s assets and revenues:

Key People & Top 10 Shareholders

The company is comprised of credible experienced people who believe in the company:

Ronald (Ron) M. Bachmeier- President & CEO, Director (59 years old, not independent):

- Owns 0.44% of the voting shares of ZCL

- Served as the CFO of Xerxes Corporation since 1986

- Became COO of US Operations after ZCL’s acquisition of Xerxes (2007)

COO of ZCL since February 2008; became President & CEO, and Director of ZCL in 2012. - Holds Chartered Public Accountant (CPA) designation, Bachelor of Science degree in Business Administration from the University of North Dakota

- Serves on the board of the American Composites Manufacturers Association (ACMA)

Anthony (Tony) P. Franceschini – Independent Chair of the Board (66 years old):

- Owns 0.26% of the voting shares of ZCL

- Became a director in 2009 and Chairman of the Board in 2012

- Worked at a global Engineering and Design company, Stantec Inc., (STN:TSX) since 1978 & served as the CEO of the company from 1998 until retirement in 2009

- Serves as a Director with Esterline Technologies Corporation (ESL:NYSE)

- Serves as a Director with Aecon Group (ARN:TSX) and two other private companies

Darcy Morris – Independent Director (35 years old):

- Owns 4.91% of the voting shares of ZCL

- Co-founder of Ewing Morris (independent investment manager)

- Previously portfolio manager at MacDougall, MacDougall & MacTier (2009 to 2011)

- Serves on the boards of numerous private companies; graduate of Queens University

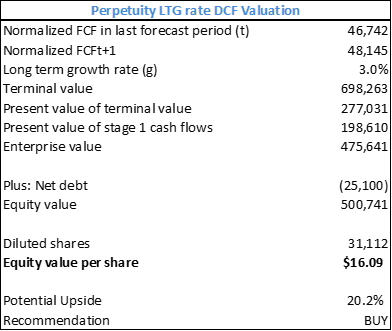

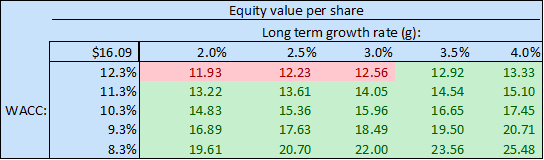

Valuation

DCF

Scenario Analysis

I have built 3 scenarios (Base, Best, Worst) based on revenue growth, gross profit margin, general & administrative margin, to generate 10Y forecast and arrive at implied share price.

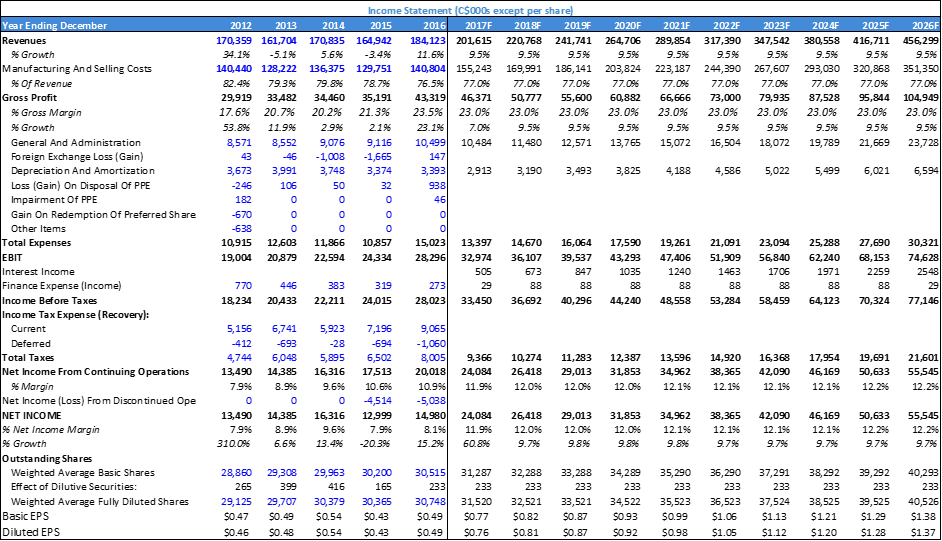

Free Cash Flow to the Firm (FCFF)

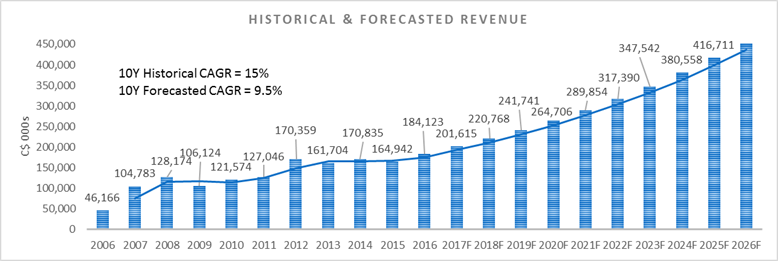

The company generated an estimated FCFF margin of 15% in 2016 due to strong operational performance. ZCL is estimated to grow FCFF at 5.3% CAGR at 10.6% FCFF 10Y margin, triggered by positive strong revenue growth, sustaining cost and hence profit margins, and modest CapEx requirements. The DCF model assumes terminal growth rate of 3% and WACC of 10.2% to calculate PV of FCFF.

DCF Conclusion

The Base case implied share price is estimated at $16.09 with a possible upside of 20%. In 2016, ZCL also had a dividend yield of approximately 8.8% in 2016 including special dividend, with a 3.4% regular dividend yield. With an estimated 3% dividend yield in 2017, that implies ~ 23% total return. The Best case scenario implies a total return of ~ 36% while a Worst case scenario implies a total return of ~ 7%.

Exit EBITDA Multiple Approach

In addition, I modeled an Exit EBITDA Multiple model assuming 11x exit multiple (current EV/EBITDA of 11.7x) on 2026F EBITDA to estimate terminal value. The EV hence consists of the 10Y forecasted FCFF and PV of the terminal value. I estimated an implied share price of $18.85 with a 31.9% upside potential.

Risks & Challenges

The company has a large customer base in the downstream retail oil and gas industry. As a result, if investment spending by these companies is not sustained or growing, the continued revenue growth prospects of the company will be at risk. The company in its defense regarding this has a diverse customer base with only 1 customer with greater than 10% of the total accounts receivable as of Q1 2017, the collectability of which is not at risk, as per management expectation. Since oil prices has damped starting June 2014, overall spending has reduced in oil and gas sector. Although the challenges brought by the oil price crash has not gone away and companies are cautious, situation has improved since then.

The fact that company’s products are more environmentally friendly, longer lasting, better quality and less expensive in some cases to install than steel, concrete or other FRP manufacturers are key selling points. With the new US administration, if environmental regulations are laxed, the future robust prospects for ZCL might deteriorate. This is very much an uncertainty we all have to wait and see how it plays out.

Water segment in both US & Canada has potential high growth prospects, with growth potential in Fuel markets in US as well. However, I am of the belief that is so for the next 10 years. Would the high growth story continue beyond that period in this unique business, that is questionable and might not be so. I do feel that there is a cyclicality risk to the business and should be taken into account. The recent and prospective growth is a result of the cycle of aging tanks that are 20-30 years old or more that were installed starting 1980s.

Conclusion

ZCL has become a market leader gobbling up market share in the underground storage tank space since its beginnings 30 years ago. It has gone through various shifts including forming an increasing portion of its revenue base from US, decreasing portion from Canada; and albeit small but increasing international revenues.

It holds an estimated 60% market share for its fuel category for the overall North American market, which makes its profitability sustainable. Given the aging storage tanks that were installed in the 1980s and the potential environmental issues related to leaking, in addition to the growing entry of big box retailers into the retail fuel selling space makes its highest generating mature segment still lucrative. The company’s water segment is potentially the next highest growing segment as management expects and has potential to grow due to diversified customer base both in Canada and US. The oil and gas sector has faced challenges since the oil price due to reduced new CapEx spending from the industry players but remains important to the business with maintenance CapEx spending and potential new spending at the new normal low oil prices.

The company looks expensive with a P/E of ~ 26x based on 2016 earnings. However, considering the company’s overall dominant industry position, high expected revenue growth, robust return metrics, attractive balance sheet and shareholder focused management, it is a fundamentally strong company. I reiterate a BUY recommendation with a potential share price upside of 20% and dividend yield of 3%.

APPENDIX

Leave a comment